Since the UK left the EU, importing goods from Europe has become more complex. If you’re bringing goods into the UK from the EU, the short answer is: yes, you have to pay import VAT.

The rules depend on the value of the goods, who’s buying them, and how the shipment is structured. Post-Brexit, there are more ways to manage when and how you pay VAT, because postponed VAT accounting can also be used.

In this post, we’ll explain when import VAT applies, and what options are available to reclaim it.

Creative Takeaways

- Import VAT applies to goods from the EU post-Brexit, just like goods from non-EU countries.

- If the goods are worth more than £135, import VAT is charged at the UK border.

- VAT-registered businesses can use Postponed VAT Accounting (PVA) to declare VAT on their VAT Return instead of paying it immediately.

- The import VAT is calculated on the total customs value, including item cost, shipping, and insurance.

- Zero-rated goods must still be declared, even though no VAT is charged.

Table of contents

1. What is import VAT?

Import VAT is a tax you pay when goods enter the UK from other countries. It’s charged at the same rate as if you bought the goods in the UK.

In most cases, the import VAT rate is 20%. HMRC collects this tax to make sure that imported goods don’t have an unfair price advantage over goods sold domestically.

Post-Brexit the UK treats EU imports the same way as goods from the rest of the world. Import VAT is normally paid before the goods are released from customs. But, if you’re VAT-registered, you may be able to account for it through your VAT return using postponed VAT on accounting (PVA) – more on that later!

Domestic VAT vs import VAT

Domestic VAT is the tax you charge or pay on goods and services sold within the UK. It’s added to business transactions and collected by VAT-registered businesses on behalf of HMRC.

Import VAT is different than domestic VAT. Import VAT is applied when goods cross the UK border. Instead of being part of a sale, it’s part of a customs process. You don’t pay it to your supplier – you pay it (or account for it) when goods arrive in the UK.

2. When do you pay VAT on imported goods from the EU?

You usually pay import VAT when goods enter the UK from the EU. This applies even if you’re buying for business or personal use.

The most important factor here is the value of the goods.

If the total value of a consignment is over £135, import VAT will apply at the border.

For goods at or below £135, the rules change.

In most B2C (business-to-consumer) cases, VAT is charged at the point of sale instead. The seller is responsible for collecting UK VAT and paying it to HMRC.

For B2B (business-to-business) transactions, where both the buyer and seller are registered for VAT, the buyer usually accounts for VAT using postponed VAT accounting.

If you’re not sure about which one applies to you, feel free to reach out – it’s free!

Your VAT responsibility depends on your role:

- Importer: Usually pays VAT at the border or through their VAT Return.

- Seller: May need to register for UK VAT if selling directly to UK customers.

- Marketplace or courier: Often responsible for collecting VAT in cross-border eCommerce.

Customs duties are completely different and separate from VAT, but they may also apply depending on the type of goods.

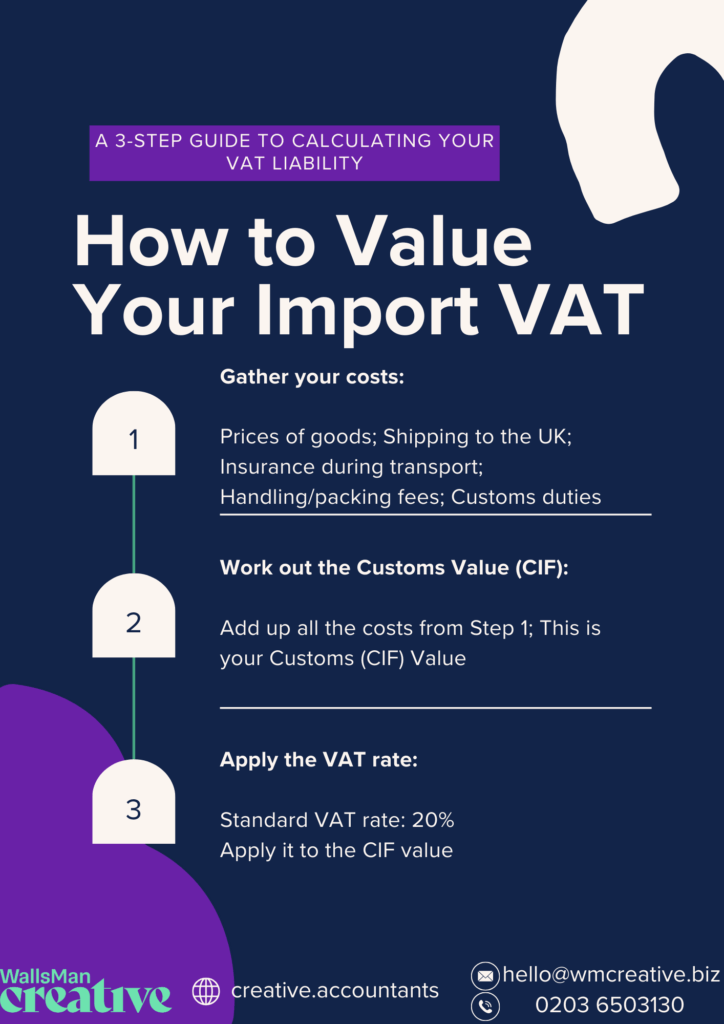

3. How to value your import VAT

If you want to calculate how much import VAT you owe, you need to work out the customs value of the goods.

HMRC has its own guidance for how to value goods for import VAT that you can check out on their official website.

This price that you calculate isn’t just the price you paid. It also includes extra costs like shipping and insurance. This total is often called the CIF value (Cost, Insurance and Freight).

Here’s what you have to include in your customs value:

- The price you paid for the goods

- Shipping costs to the UK

- Insurance during transport

- Any handling or packing fees

- Customs duties (if they apply)

Once you have that total, apply the correct VAT rate – that is usually 20%.

It’s complicated, so let’s see it through an example:

You import goods from Germany worth £1,000. Shipping costs are £100, and insurance adds another £20. There’s no customs duty on this item.

That gives you a total customs (CIF) value of £1,120. VAT is charged at 20%, so the import VAT due is £224.

4. Postponed VAT accounting (PVA)

The existing rules for imports from non-EU countries now apply to imports from the EU, but with some changes.

The UK government has introduced postponed VAT accounting (PVA) for import VAT on goods brought into the UK with effect from 1 January 2021. This means that UK VAT-registered businesses importing goods to the UK are able to account for import VAT on their VAT return, rather than paying import VAT on or soon after the time that the goods arrive at the UK border.

This can give businesses a cashflow benefit.

This important relaxation applies to imports from the EU and non-EU countries. Postponed accounting can be used by all VAT registered business in the UK and no separate application is required.

However, customs declarations and the payment of any other duties are still required. Customs duty (tariffs) apply to some goods and excise duties continue to apply to tobacco, alcohol and certain energy products.

5. What about zero-rated VAT?

Some goods are zero-rated for VAT. This includes items like children’s clothes, books, and most food.

If you’re importing zero-rated goods, you still need to declare them, but no VAT will be charged at the border. The same rules for customs value and paperwork still apply, and you may still need to pay customs duties if applicable.

Being zero-rated doesn’t mean exempt – it means the goods are taxable, just at a 0% rate, which keeps the in the VAT system.

6. Ask VAT experts for expert tips

Post-Brexit complicated things a bit with postponed VAT accounting. There’s more to look out for now, and you have to keep clear, well-organised records of all import transactions.

Don’t worry if you don’t know all the answers for how and when you need to pay VAT on imported goods from the EU or from other countries. We’re here to help.

Book a free consultation to speak with us!